In 2010, I was a mom-to-be with one child already at home and a marriage quietly unraveling. I knew I had to secure a future for my children and myself. So, while pregnant with my second child, I made the leap and enrolled in nursing school. I borrowed around $30,000 in federal student loans to earn my associate degree in nursing, graduated, passed my boards, and began working immediately. For a while, things felt like they were on track.

By 2016, I was encouraged to advance my education and pursue my BSN. That’s when I heard about Chamberlain University. It sounded like the perfect fit — I was told I could finish in as little as six months, that I’d only pay one semester at a time, and that there would be no out-of-pocket costs. The admissions team made it sound like a streamlined path forward. It wasn’t.

Eighteen months later, I was nowhere near graduation, and my debt had ballooned by another $45,000, bringing my total student loan balance to $75,000 — and I still didn’t have a degree. Every time I asked how close I was to finishing, I was told “just another semester or two.” The promises felt endless, vague, and increasingly disheartening.

What’s worse: before I even began the program, I had emailed asking about credentialing in my state and clinical eligibility. The response I got was delayed and full of mixed messages. One advisor assured me they were “working through compliance,” but I was never given a definitive answer. That means I was never sure the clinicals I would complete — or the degree itself — would even be recognized by my state’s Board of Nursing. That ambiguity is one of many red flags I flagged in my Borrower Defense application.

By 2018, I had enough. I was exhausted by the emotional and financial toll and withdrew from the program just a few classes short of completing my BSN.

Since then, I’ve been steadily working as a nurse, raising my kids, and doing what so many borrowers do — making monthly payments while watching the interest grow faster than I could keep up. I never missed payments. I never defaulted. But it still didn’t feel like progress.

Then this year, I finally decided to buy a home — something I never thought possible as a single mom buried in debt. I was approved and in the final stages of closing. But when my lender pulled an updated credit report, a new collection for $1,115 had mysteriously appeared. It was from Chamberlain.

This debt had never shown up before. It wasn’t on my May report, but suddenly it showed up in June — just two months before it was scheduled to fall off my credit report entirely (August, 2025). With that, my mortgage approval was revoked.

I had the option to pay it off. But honestly? I couldn’t stomach paying another cent to a school that left me with no degree, unclear clinical credentials, and a mountain of debt. So I let the home go.

In the meantime, I’ve discovered resources I wish I’d known about years ago. I submitted an application for Public Service Loan Forgiveness (PSLF) — something I assumed I wasn’t eligible for because I was on a standard repayment plan. But I’ve now been told I have 144 qualifying payments on my original loans and around 70 qualifying months on the second set tied to Chamberlain. I'm now working on certifying my employment to formalize that progress. One where I have had 10, yes 10 failed submissions due to silly clerical errors.

I also submitted a Borrower Defense to Repayment application — twice. The first time, I felt unsure. The second time, I attached emails and evidence showing the misleading guidance, false promises about timelines and costs, and unclear accreditation issues. I now believe my application is materially complete, without any assurances or timeline. Promises from others shared experiences that this process will in fact take me years if not decades. With no legal representation, or protections like the earlier class action members. Feeling alone, and kind of like a loser. I just wish I had known about it sooner.

I know my case might be denied. I know this might take months — or years- or decades. But I’m not giving up. Because this isn’t just my story. It’s the story of so many of us who tried to do everything right… and are still paying for it.

Kashana Cauley’s second novel, The Payback (out July 15, 2025), might read like a brilliantly absurd heist movie—but its critique of debt peonage, surveillance capitalism, and broken educational promises is dead serious. With its hilarious yet harrowing depiction of three underemployed retail workers taking on the student loan-industrial complex, The Payback arrives not just as a much-anticipated literary event, but as a cultural reckoning.

The protagonist, Jada Williams, is relentlessly hounded by the “Debt Police”—a dystopian twist that, while fictional, feels terrifyingly close to home for America’s 44 million student debtors. But instead of accepting a life of financial bondage, Jada and her mall coworkers hatch a plan to erase their student debt and strike back against the system that sold them a future in exchange for permanent servitude.

This wild caper—praised by Publishers Weekly, Bustle, The Boston Globe, and others for its intelligence and audacity—may be fiction, but it echoes the real-life story of one bold man who did exactly what Jada dreams of doing.

The Legend of Papas Fritas

In the mid-2000s, a Chilean man known only by his pseudonym, Papas Fritas (French Fries), pulled off one of the most radical and symbolic acts of debt resistance in modern history. A former art student at Chile’s prestigious Universidad del Mar—a private for-profit institution later shut down for corruption and fraud—Papas Fritas discovered that the university had falsified financial documents to secure millions in profits while leaving students in mountains of debt.

His response? He infiltrated the school’s administrative offices, extracted records documenting approximately $500 million in student loans, and burned them. Literally. With no backup copies.

He then turned the ashes into an art installation called “La Morada del Diablo” (The Devil’s Dwelling), displayed it publicly, and became an instant folk hero. For many Chileans, who had taken to the streets in the early 2010s protesting an exploitative and privatized higher education system, Papas Fritas was more than a trickster—he was a vigilante philosopher, an artist of revolt.

His act raised questions that still haunt us: What is the moral value of debt acquired through deception? Should the victims of predatory institutions be forced to pay for their own exploitation?

Fiction Meets Resistance

In The Payback, Cauley’s characters don’t just want debt relief—they want retribution. And like Papas Fritas, they understand that justice in an unjust system may require transgression, even sabotage. Cauley, a former Daily Show writer and incisive New York Times columnist, doesn’t shy away from this. Her prose is electric with rage, joy, absurdity, and clarity.

She also knows exactly what she’s doing. Jada’s plan to eliminate debt isn’t merely about numbers—it’s about dignity, possibility, and reclaiming a future that was sold for interest. Cauley’s fiction, like Papas Fritas’s fire, is not just a spectacle—it’s a warning, and a dare.

In an America where student debt totals over $1.7 trillion, where debt servicers act like bounty hunters, and where the promise of higher education has become a trapdoor, The Payback delivers catharsis—and inspiration.

Hollywood, take note: this story demands a screen adaptation. But more importantly, policymakers, debt collectors, and university administrators should take heed. The people are reading. And they’re getting ideas.

Preorder The Payback

Signed editions are available through Black-owned LA bookstores Reparations Club, Malik Books, and Octavia’s Bookshelf. National preorder links are now live. Read it before the Debt Police knock on your door.

Because as both Cauley and Papas Fritas remind us: sometimes, the only moral debt is the one you refuse to pay.

On June 26th, the US Department of Education was brought to the Ninth District Court (and Judge Alsup) to show how many the Borrower Defense to Repayment cases that have been resolved per court order.

While we wait for a transcript of the latest episode of Sweet v McMahon, what we can tell you is that the Trump government continues to drag its feet in paying back debtors who have been defrauded.

According to Theresa Sweet:

“We really need Borrower Defense applicants included in both the full and post class of Sweet to send any denials to the Project on Predatory Student Lending. It’s important for the legal team to be able to track this and make sure there are no patterns of boilerplate denials or mass denials. It’s also really important to remember that if a Sweet class or post class member gets a denial it should include a Revise and Resubmit notice, which *must* be resubmitted on time or the denial becomes final unless the person takes it to court on their own.”

The next episode of Sweet v. McMahon (formerly Sweet v. Cardona), "THE CLOCK IS TICKING," will premiere on Thursday, June 26, 2025.

Judge Alsup is BACK. He wants updates. He wants answers. And he’s asking one thing — will the deadlines be met? Join in for the next drama episode in this six-year battle for justice!

Deets Below:

Sweet v. McMahon: The Clock Is Ticking Date: Thursday, June 26, 2025 Time: 2:00 PM ET / 11:00 AM PT

Borrowers are still waiting. Judge Alsup wants answers. The DOE is back in court. Will justice finally be delivered? Tune in. Speak up. This hearing will be fire!

In a modest but potentially revealing inquiry, the Higher Education Inquirer has submitted a Freedom of Information Act (FOIA) request to the U.S. Department of Education asking for a count of the number of student loans discharged in bankruptcy from 1965 to 2024. The request, dated June 10, 2025, was acknowledged the same day by the Department’s FOIA Service Center under FOIA Request No. 25-03954-F.

“The Higher Education Inquirer is requesting a count of the number of student loans forgiven in bankruptcy per year from 1965 to 2024.”

It’s a simple request with profound implications. While the nation debates student loan forgiveness through executive action and legislative reforms, the forgotten path of bankruptcy discharge—once a legally viable option for debt relief—has been quietly buried over the past several decades.

A Timeline of Restriction: The Death of Bankruptcy Relief

When the Higher Education Act of 1965 established federal student loans, they were treated like other forms of consumer debt. Borrowers could, in principle, discharge them through bankruptcy just like credit card debt or medical bills.

But that began to change in the late 1970s, as concerns over potential abuse of the system gained traction in Congress. In 1976, a new law prohibited the discharge of federal student loans in bankruptcy within the first five years of repayment unless the borrower could prove “undue hardship”—a vague standard that was rarely met.

From there, the restrictions only grew tighter:

1990: The waiting period for dischargeability was extended to seven years.

1998: The option to discharge federal student loans in bankruptcy for any reason other than “undue hardship” was eliminated entirely. This meant student loan borrowers had to meet the strict and often inaccessible hardship standard at all times.

2005: Under the Bankruptcy Abuse Prevention and Consumer Protection Act (BAPCPA), Congress extended the “undue hardship” requirement to most private student loans as well—effectively removing nearly all forms of bankruptcy relief from the table for student debtors.

These changes did not result from clear evidence of widespread abuse. Rather, they were fueled by myths of “deadbeat graduates” walking away from their obligations and by lobbying from banks, guaranty agencies, and debt collection firms that profited from non-dischargeable debt. Meanwhile, evidence of hardship among borrowers grew, especially for those who attended predatory for-profit colleges or dropped out without a degree.

The Brunner Barrier

The biggest obstacle for borrowers remains the so-called “Brunner test,” a three-prong legal standard established in a 1987 court case, Brunner v. New York State Higher Education Services Corp. It requires borrowers to prove:

They cannot maintain a minimal standard of living if forced to repay the loans,

Their financial situation is unlikely to improve, and

They made a good-faith effort to repay the loans.

Many judges interpreted these criteria narrowly, creating a virtually insurmountable hurdle. Borrowers with severe disabilities, advanced age, or long-term unemployment have been denied relief even when destitute.

What We Still Don’t Know

Despite these legal developments and the hardship they created, data on how many people have succeeded in discharging their student loans through bankruptcy remains remarkably scarce. Advocacy groups and journalists have long questioned why no federal agency tracks this information in a clear, public-facing format.

That’s what prompted the Higher Education Inquirer’s FOIA request—an effort to establish a factual baseline. We asked the Department of Education for an annual count of bankruptcy discharges involving student loans over a 60-year period, from 1965 to 2024.

The Bureaucratic Wall

According to the Department’s FOIA Service Center, the average processing time for such requests is currently 185 business days—about nine months. While the Department did not ask for clarification immediately, it reserves the right to do so within ten business days. Failure to respond to such a request would result in administrative closure of the FOIA—yet another form of delay that keeps the public in the dark.

This bureaucratic stonewalling is part of a larger pattern. While the Department of Education has been quick to announce student loan forgiveness programs under executive orders or settlement agreements, it remains reluctant to shine a light on longstanding failures—especially the erosion of legal remedies like bankruptcy.

A Step Toward Truth and Accountability

The public deserves a clear view of the history and consequences of stripping bankruptcy protections from student borrowers. It’s not just a legal matter—it’s a story of systemic neglect, political pressure, and financial exploitation. Without access to historical data, reform remains a guesswork operation and accountability remains elusive.

We at the Higher Education Inquirer will continue to press for answers. If and when the FOIA request is fulfilled, we will publish the data and conduct a thorough analysis, year by year. We believe that exposing the truth about student loan bankruptcy isn’t just a matter of curiosity—it’s a step toward justice.

If you have experience with student loan bankruptcy, data that could assist our investigation, or simply want to share your story, contact us at gmcghee@aya.yale.edu.

The Higher Education Inquirer has received information today from the US Department of Education about Borrower Defense to Repayment claims. Here are the results from ED FOIA 25-02047-F.

Although President Donald J. Trump last month signed an executive order

directing Secretary of Education Linda McMahon “to the maximum extent

appropriate and permitted by law, take all necessary steps to facilitate

the closure of the Department of Education,” and although DOGE efforts

and layoffs have cut the Department staff by half, the Department

announced today that it will embark on an extensive round of meetings to

draft new regulations governing student financial aid.

Unlike most federal agencies, the Department is generally required to

engage in an elaborate process called negotiated rulemaking before it

can issue or cancel regulations. This has meant — on issues from campus

sexual assault to performance standards guarding against predatory

college abuses — years of public hearings, formal convenings of

rulemaking panels, written public comments and meetings on draft

regulations, and more. It also has produced a decades-long ping pong

match of final regulations made by one party and overwritten by the

other, from the Obama to Trump I to Biden, followed by years of court

challenges.

The first Trump administration

staffed its higher education jobs with former executives of predatory

for-profit colleges, and they eliminated both regulations and

enforcement efforts aimed at protecting students and holding predatory

schools accountable.

Today’s notice,

signed by James P. Bergeron, Acting Under Secretary of Education, says

the first round of Trump II negotiated rulemaking will likely include

consideration of Public Service Loan Forgiveness and other loan

repayment programs “or other topics that would streamline current

federal student financial assistance programs.”

Other language in the notice suggests the Department may go deep,

perhaps working to cancel the Biden rules creating performance standards

for for-profit and career college programs (the gainful employment

rule) and providing debt relief for students scammed by their colleges

and government recoupment of funds from dishonest schools (the borrower

defense rule). The notice opines that current regulations “may be

inhibiting innovation and contributing to rising college costs” and that

it wants to “streamline” the rules “while maintaining or improving

program integrity and institutional quality.” “Innovation,” while a

great thing for education when it can really happen, has been a buzzword

used by the for-profit college industry to fight against rules aimed at

protecting against predatory programs. Gutting the Biden rules would

increase the vulnerability of both students and taxpayers to billions in

waste, fraud, and abuse from deceptive, poor quality schools — even

though the stated purpose of DOGE is to halt government excess.

When pro-student Democratic members of the House of Representatives

held a press conference outside the Department headquarters yesterday

after they met with McMahon to discuss such concerns, she followed them.

But she quickly fled when Rep. Mark Takano (D-CA) asked her when she would shut down the building.

The Department’s rulemaking process begins with public hearings on

April 29 and May 1, the first in-person at Department headquarters and

the second online. Advocates for students and taxpayers should register to speak and show up to make their voices heard.

[Editor's note: This article originally appeared on Republic Report.]

The federal government is a sh*t show right now. From ICE abductions of pro-Palestine college students to proposed cuts to Social Security and Medicaid, the Trump administration is wreaking havoc on all of our communities.

We want to take a moment and specifically talk about student debt and higher education — work that we’ve been doing for a while now. Here’s some of what we know, what we think, and what we should do:

In recent days, the Trump administration issued an executive order to dismantle the Department of Education. Legally, this cannot be done without Congress, but in practice, this means most of the staff was simply fired. We talked a little bit about what that means for student debtors in this Twitter thread. In short, this makes the student debt crisis much worse.

Shortly after that, Trump ordered the entire federal student debt portfolio — all $1.7 trillion — to be moved from the Department of Education to the Small Business Administration (SBA). The Small Business Administration is another agency within the federal government. That means our collective creditor would still be the federal government. But will this move actually happen? Will our federal student loans somehow end up privatized? There is a LOT up in the air right now, and the short answer is we don’t know exactly what will happen, but we as debtors should remain nimble so we can exercise our collective power when we need to. Moving our student debt from the Department of Education to the SBA would be 1) illegal 2) administratively and practically difficult 3) lead to possible errors with your account.

If you haven’t already, we still highly recommend going to studentaid.gov and finding your loan details and downloading and/or screenshotting your history.

The traditional infrastructure we have long suggested debtors utilize to solve problems with their student debt — the Consumer Financial Protection Bureau (CFPB), the FSA ombudsman team, etc — have either been undermined or outright destroyed. This means there are fewer and fewer ways for us, student debtors, to get answers to problems with our student debt accounts. But we shouldn’t let Congress off the hook — we should make student loans Congress’ problem. They’re elected to serve us and it’s their job to attend to your needs.

Lastly, we want to talk about what we mean when we say Free College. Student debt has ruined lives, and will continue to as long as it exists. We shouldn’t have to borrow to pay for college — in fact, we shouldn’t have to pay at all. It should be free. And that’s what we’re fighting for. But our vision for College For All doesn’t stop at tuition-free — it means ICE and cops off campus; it means paying workers, faculty and staff a living wage; it means standing up for free speech; it means ending domestic and gender based violence on campus; and it means universities that function as laboratories for democracy and learning, not as laboratories for landlords and imperialism.

On April 17th, Debt Collective is co-sponsoring the National Higher Education Day of Action to demand our vision of College For All and oppose the hell the Trump administration is causing right now. Find an event near you HERE to participate — or start an event on your own!

And THIS SATURDAY – April 5th –we’re taking to the streets with hundreds of thousands of people across the country to tell Trump and Musk “Hands Off Our Democracy!” They’re stripping America for parts, and it's up to us to put an end to their brazen power grab. This will be one of the largest mass mobilizations in recent history — and we need you in the streets with us. There are hundreds of actions planned, find one to join near you HERE.

Whatever happens in the future, we will be more likely to win if we gird ourselves with each other’s stories and experiences so we can fight together. This is why we built a debtors’ union — the only virtual factory floor for debtors. Debt acts as a discipline and keeps people from joining the struggle for things we care about — but we can increase our numbers and build power by canceling unjust debts. We all share the same creditor and we need to stay connected to one another. Forward this email to a friend or family member and tell them to join the union and our email list so we can stay connected.

The Higher Education Inquirer has recently received a Freedom of Information (FOIA) response regarding student loan debt held by former Liberty University students. The FOIA was 25-01941-F.

The Higher Education Inquirer has recently received a Freedom of Information (FOIA) response regarding student loan debt held by former Liberty University students. The FOIA was 25-01939-F.

The Higher Education Inquirer has recently received a Freedom of Information (FOIA) response regarding student loan debt held by former DeVry University students. The FOIA was 25-01942-F.

The U.S. student loan system, now exceeding $1.7 trillion in debt and affecting over 40 million borrowers, is facing significant challenges. As political pressures rise, the management of student loans could be significantly altered. A combination of potential privatization, the elimination of the U.S. Department of Education (ED), and a new role for the Department of the Treasury raises critical questions about the future of the system.

U.S. Department of Education: Strained Resources and Outsourcing

The U.S. Department of Education (ED) is responsible for managing federal student loan servicing, loan forgiveness programs, and borrower defense to repayment (BDR) claims. However, ED has faced ongoing issues with understaffing and inefficiency, particularly as many functions have been outsourced to contractors. Companies like Maximus (including subsidiaries like AidVantage) manage much of the administrative burden for loan servicing. This has raised concerns about accountability and the impact on borrowers, especially those seeking loan relief.

In recent years, ED has also experienced staff reductions and funding cuts, making it difficult to process claims or maintain high-quality service. The potential for further cuts or even the elimination of the department could exacerbate these problems. If ED’s role is diminished, other entities, such as the Department of the Treasury, could assume responsibility for managing the student loan portfolio, though this would present its own set of challenges.

Potential for Privatization of the Student Loan Portfolio

One of the most discussed options for addressing the student loan crisis is the privatization of the federal student loan portfolio. Under previous administration discussions, including those during PresidentTrump’s tenure, there were talks about selling off parts of the student loan portfolio to private companies. This would be done with the aim of reducing the federal deficit.

In 2019, McKinsey & Company was hired by the Trump administration to analyze the value of the student loan portfolio, considering factors such as default rates and economic conditions. While the report's findings were never made public, the idea of transferring the loans to private companies—such as banks or investment firms—remains a possibility.

The consequences of privatizing federal student loans could be significant. Private companies would likely focus on profitability, which could result in stricter repayment terms or less flexibility for borrowers seeking loan forgiveness or other relief options. This shift may reduce borrower protections, making it harder for students to challenge repayment terms or pursue loan discharges.

The Department of the Treasury and its Potential Role

If the U.S. Department of Education is restructured or eliminated, there is a possibility that the Department of the Treasury could step in to manage some aspects of the student loan portfolio. The Treasury is responsible for the country’s financial systems and debt management, so it could, in theory, handle the federal student loan portfolio from a financial oversight perspective.

However, while the Treasury has experience in financial management, it lacks the specialized knowledge of student loans and borrower protections that the Department of Education currently provides. For example, the Treasury would need to find ways to process complex Borrower Defense to Repayment claims, a responsibility ED currently manages. In 2023, over 750,000 Borrower Defense claims were pending, with thousands of claims related to predatory practices at for-profit colleges such as University of Phoenix, ITT Tech, and Kaplan University (now known as Purdue Global). Additionally, some of these for-profit schools were able to reorganize and continue operating under different names, further complicating the situation.

The Treasury could also contract out loan servicing, but this could increase reliance on profit-driven companies, possibly compromising the interests of borrowers in favor of financial performance.

Borrower Defense Claims and the Impact of For-Profit Schools

A large portion of the Borrower Defense to Repayment claims comes from students who attended for-profit colleges with a history of deceptive practices. These institutions, often referred to as subprime colleges, misled students about job prospects, program outcomes, and accreditation, leaving many with significant student debt but poor employment outcomes.

Data from 2023 revealed that over 750,000 Borrower Defense claims were filed with the Department of Education, many of them against for-profit institutions. TheSweet v. Cardona case showed that more than 200,000 borrowers were expected to receive debt relief after years of waiting. However, the process was slow, with an estimated 16,000 new claims being filed each month, and only 35 ED workers handling these claims. These delays, combined with the uncertainty around the future of ED, leave borrowers vulnerable to prolonged financial hardship.

Lack of Transparency and Accountability in the System

While the U.S. Department of Education tracks Borrower Defense claims, it does not publish institutional-level data, making it difficult to identify which schools are responsible for the most fraudulent activity.

In response to this,FOIA requests have been filed by organizations like the National Student Legal Defense Network and the Higher Education Inquirer to obtain detailed information about which institutions are disproportionately affecting borrowers.

The lack of transparency in the system makes it harder for borrowers to make informed decisions about which institutions to attend and limits accountability for schools that have harmed students. If the Treasury or private companies take over management of the loan portfolio, these transparency issues could worsen, as private entities are less likely to prioritize public accountability.

Conclusion

The future of the U.S. student loan system is uncertain, particularly as the Department of Education faces the potential of funding cuts, staff reductions, or even complete dissolution. If ED’s role diminishes or disappears, the Department of the Treasury could take over some functions, but this would raise questions about the fairness and transparency of the system.

The possibility of privatizing the student loan portfolio also looms large, which could shift the focus away from borrower protections and toward financial gain for private companies. For-profit schools, many of which have a history of predatory practices, are responsible for a disproportionate number of Borrower Defense claims, and any move to privatize the loan portfolio could exacerbate the challenges faced by borrowers seeking relief from these institutions.

Ultimately, there is a need for greater transparency and accountability in how the student loan system operates. Whether managed by the Department of Education, the Treasury, or private companies, protecting borrowers and ensuring fairness should remain central to any future reforms. If these issues are not addressed, millions of borrowers will continue to face significant financial hardship.

What happens now with the US Department of Education now that Elon Musk claims that it no longer exists? It's hard to know yet, and even more difficult after removing career government workers that we have known for years.

We are saddened to hear of contacts we know who have been fired: hard working and capable people, in an agency that has been chronically understaffed and politicized.

We also worry for the hundreds of thousands of student loan debtors who have borrower defense to repayment claims against schools that systematically defrauded them--and have not yet received justice.

And what about all those FAFSA (financial aid) forms for students starting and continuing their schooling? How will they be processed in a timely manner?

[Editor's note: The Higher Education Inquirer is presenting this press release for information only. This is not an endorsement of the organizations mentioned in article.]

NEW YORK, Jan. 27, 2025 /PRNewswire/ -- A new survey, The Student Debt Dilemma: The Impact on Financial Milestones, released today by Laurel Road,

a digital banking platform of KeyBank with specialized offerings for

healthcare and business professionals, in partnership with Luminary, a global professional education and networking platform, and conducted by Kantar, reveals the obstacles borrowers face in managing student loan repayment – from information overload to confidence gaps.

The survey of 1,714 U.S. adults found that 70% felt overwhelmed

when navigating repayment options, with 76% of respondents experiencing

an overload of information, underscoring the significant anxiety and

confusion faced by borrowers. These findings underscore the impact of

debt on milestone life events as well as the difficulty of navigating an

intricate repayment system.

Challenges amid Regulatory Changes Recent

changes and fluctuating regulations in the federal student loan system

have created ongoing uncertainty for borrowers navigating their

repayment options. According to the survey, 82% of respondents aged 25

to 44 reported feeling "unsure what plans/options are right for me,"

demonstrating the ever-changing environment as a primary pain point.

Additionally, 58% of individuals in the combined 25-44 age group

reported feeling moderately overwhelmed – a significantly higher

percentage compared to the 45 and older age group (34.8%)– emphasizing

the unique challenges younger borrowers face in making informed

decisions.

Low Levels of Confidence in Repayment Strategies Navigating

student loan repayment is a complicated process, requiring borrowers to

understand available options, conduct thorough research to identify

loan management opportunities, and select the most appropriate repayment

plan or forgiveness program.

According to the survey, 26% of

respondents noted that they did not have a plan for managing their

student loans, while 20% indicated they planned to use Federal

Income-Driven Repayment, and 15% intended to pursue the Public Service

Loan Forgiveness (PSLF) program.

Confidence is another major

concern, as 61% of borrowers surveyed reported a lack of confidence in

their repayment strategies while only 13% reported feeling confident in

their approach.

"This study confirms everything we believed to be

true relating to confusion and lack of confidence student loan borrowers

face today. Information overload and ambiguity has left borrowers

yearning to understand the repayment and forgiveness options available

to them, and to receive this information in a clear, concise manner,"

said Alyssa Schaefer, General Manager and

Chief Experience Officer at Laurel Road. "Laurel Road is at the

forefront of helping borrowers gain their confidence by offering free

consultations with student loan experts who can help them make informed

decisions, navigate the complexities of repayment, and build the

confidence needed to reach their financial goals – ultimately securing

their financial futures."

Impact of Student Loans on Financial Futures In

addition to being difficult to navigate, the student loan landscape has

the potential to largely affect borrowers' overall financial well-being

and long-term goals. The survey revealed that student loan debt has

delayed significant life milestones for respondents, with borrowers

reporting the following impacts:

79% struggle to save for emergencies or retirement

75% are unable to invest for the future

52% are unable to purchase a home

35% are postponing starting a family

"Luminary has seen first-hand the impact of student loan debt on

our Members, from a lack of understanding about available options to

the affect it has on an individual's mental health due to stress, worry

and anxiety, " said Luminary founder and CEO Cate Luzio. "While this

isn't new information for us, given our longstanding partnership

with Laurel Road, we felt this survey was necessary to demonstrate the

real toll it's taking on people. As we prepare for a new administration

in 2025, this is top of mind as we continue developing programming to

educate and inform those affected."

Delays in life milestones not

only affect individual wellbeing but also pose broader risks to economic

stability and financial security. Through online resources and student loan consultations,

borrowers can gain confidence in understanding and tackling student

loan repayment and get on track for important financial milestones.

Methodology This survey was conducted online from September 30, 2024, to October 31,

2024 among 1,714 U.S. adults with either private or federal student

loans, by Luminary and the Kantar Profiles Respondent Hub. The primary

age group analyzed ranged from 25–44 years old, though responses were

collected from ages 18–65+. The gender breakdown of the respondents was

47% male, 51% female, 2% non-binary, and 0.4% preferring not to answer.

Statistical significance testing was completed between groups to ensure

the results did not occur by chance.

About Laurel Road Laurel

Road is a digital banking platform and brand of KeyBank that provides

tailored offerings to support the financial wellbeing of healthcare and

business professionals. Laurel Road's banking and lending solutions –

including Checking and High Yield Savings accounts, Student Loan

Forgiveness Counseling, Student Loan Refinancing, Mortgages, Personal

Loans, and more – provide our members with a simplified, personalized

experience that helps them better navigate their financial journey with

ease.

Laurel Road has reimagined banking and financial management

for physicians and dentists through Laurel Road for Doctors, a tailored

digital experience made up of banking, insights, and exclusive benefits

to provide the financial help and peace of mind they need through each

career stage. In spring of 2022, Laurel Road also launched Loyalty

Checking, the first checking account designed with nurses in mind,

furthering the company's commitment to healthcare professionals. Visit www.laurelroad.com for more information.

About Luminary Luminary is

a global membership-based professional education and networking

platform created to address and impact the systemic challenges faced by

women and underrepresented communities across all industries and

sectors, and through all phases of their professional journey. Founded

in 2018 by former finance executive Cate Luzio, Luminary is a dynamic,

gender-inclusive, multi-generational, and intersectional community

focused on creating connection, collaboration, and change through global

expert- and Member-led programming, as well as services, activations,

content, and culture. In addition, Members have access to perks and

amenities including a vast digital content library; a five-floor

building in the heart of NoMad in New York City

that is home to work and social spaces, including a rooftop restaurant;

and entree to Luminary's international Partner Network

of women-forward communities. Luminary continues to build its ecosystem

of high-touch engagement for both individual and enterprise members and

has grown to be a multimillion-dollar global B2C and B2B business with

more than 15,000 members and over 100 enterprise members. In late 2023,

the company acquired The Cru to add to its robust product offering, and

in January 2025 announced its acquisition of Hey Mama.

Notable actions the Department of Education has already taken include:

Dissolution of the Department’s Diversity & Inclusion Council, effective immediately;

Background:The Diversity & Inclusion Council was established following Executive Order 13583 under then - President Obama.President Trump has rescinded the Executive Orders that guide the Council and issued a new Executive Order, “Ending Radical and Wasteful Government DEI Programs and Preferencing,”

that terminates groups like the Diversity & Inclusion Council. DEI

documents issued and related actions taken by the Council have been

withdrawn.

Dissolution of the Employee Engagement

Diversity Equity Inclusion Accessibility Council (EEDIAC) within the

Office for Civil Rights (OCR), effective immediately and pursuant to

President Trump’s Executive Order “Ending Radical and Wasteful Government DEI Programs and Preferencing”;

Cancellation of ongoing DEI training and service contracts which total over $2.6 million;

Withdrawal of the Department’s Equity Action Plan;

Placement

of career Department staff tasked with implementing the previous

administration’s DEI initiatives on paid administrative leave; and

Identification

for removal of over 200 web pages from the Department’s website that

housed DEI resources and encouraged schools and institutions of higher

education to promote or endorse harmful ideological programs.

Rachel

Oglesby most recently served as America First Policy Institute's Chief

State Action Officer & Director, Center for the American Worker. In

this role, she worked to advance policies that promote worker freedom,

create opportunities outside of a four-year college degree, and provide

workers with the necessary skills to succeed in the modern economy, as

well as leading all of AFPI’s state policy development and advocacy

work. She previously worked as Chief of Policy and Deputy Chief of Staff

for Governor Kristi Noem in South Dakota, overseeing the implementation

of the Governor’s pro-freedom agenda across all policy areas and state

government agencies. Oglesby holds a master’s degree in public policy

from George Mason University and earned her bachelor’s degree in

philosophy from Wake Forest University.

Jonathan Pidluzny – Deputy Chief of Staff for Policy and Programs

Jonathan

Pidluzny most recently served as Director of the Higher Education

Reform Initiative at the America First Policy Institute. Prior to that,

he was Vice President of Academic Affairs at the American Council of

Trustees and Alumni, where his work focused on academic freedom and

general education. Jonathan began his career in higher education

teaching political science at Morehead State University, where he was an

associate professor, program coordinator, and faculty regent from

2017-2019. He received his Ph.D from Boston College and holds a

bachelor’s degree and master’s degree from the University of Alberta.

Chase Forrester – Deputy Chief of Staff for Operations

Virginia

“Chase” Forrester most recently served as the Chief Events Officer at

America First Policy Institute, where she oversaw the planning and

execution of 80+ high-profile events annually for AFPI’s 22 policy

centers, featuring former Cabinet Officials and other distinguished

speakers. Chase previously served as Operations Manager on the

Trump-Pence 2020 presidential campaign, where she spearheaded all event

operations for the Vice President of the United States and the Second

Family. Chase worked for the National Republican Senatorial Committee

during the Senate run-off races in Georgia and as a fundraiser for

Members of Congress. Chase graduated from Clemson University with a

bachelor’s degree in political science and a double-minor in Spanish and

legal studies.

Steve Warzoha – White House Liaison

Steve

Warzoha joins the U.S. Department of Education after most recently

serving on the Trump-Vance Transition Team. A native of Greenwich, CT,

he is a former local legislator who served on the Education Committee

and as Vice Chairman of both the Budget Overview and Transportation

Committees. He is also an elected leader of the Greenwich Republican

Town Committee. Steve has run and served in senior positions on numerous

local, state, and federal campaigns. Steve comes from a family of

educators and public servants and is a proud product of Greenwich Public

Schools and an Eagle Scout.

Tom Wheeler – Principal Deputy General Counsel

Tom

Wheeler’s prior federal service includes as the Acting Assistant

Attorney General for Civil Rights at the U.S. Department of Justice, a

Senior Advisor to the White House Federal Commission on School Safety,

and as a Senior Advisor/Counsel to the Secretary of Education. He has

also been asked to serve on many Boards and Commissions, including as

Chair of the Hate Crimes Sub-Committee for the Federal Violent Crime

Reduction Task Force, a member of the Department of Justice’s Regulatory

Reform Task Force, and as an advisor to the White House Coronavirus

Task Force, where he worked with the CDC and HHS to develop guidelines

for the safe reopening of schools and guidelines for law enforcement and

jails/prisons. Prior to rejoining the U.S. Department of Education, Tom

was a partner at an AM-100 law firm, where he represented federal,

state, and local public entities including educational institutions and

law enforcement agencies in regulatory, administrative, trial, and

appellate matters in local, state and federal venues. He is a frequent

author and speaker in the areas of civil rights, free speech, and

Constitutional issues, improving law enforcement, and school safety.

Craig Trainor – Deputy Assistant Secretary for Policy, Office for Civil Rights

Craig

Trainor most recently served as Senior Special Counsel with the U.S.

House of Representatives Committee on the Judiciary under Chairman Jim

Jordan (R-OH), where Mr. Trainor investigated and conducted oversight of

the U.S. Department of Justice, including its Civil Rights Division,

the FBI, the Biden-Harris White House, and the Intelligence Community

for civil rights and liberties abuses. He also worked as primary counsel

on the House Judiciary’s Subcommittee on the Constitution and Limited

Government’s investigation into the suppression of free speech and

antisemitic harassment on college and university campuses, resulting in

the House passing the Antisemitism Awareness Act of 2023. Previously, he

served as Senior Litigation Counsel with the America First Policy

Institute under former Florida Attorney General Pam Bondi, Of Counsel

with the Fairness Center, and had his own civil rights and criminal

defense law practice in New York City for over a decade. Upon graduating

from the Catholic University of America, Columbus School of Law, he

clerked for Chief Judge Frederick J. Scullin, Jr., U.S. District Court

for the Northern District of New York. Mr. Trainor is admitted to

practice law in the state of New York, the U.S. District Court for the

Southern and Eastern Districts of New York, and the U.S. Supreme Court.

Madi Biedermann – Deputy Assistant Secretary, Office of Communications and Outreach

Madi

Biedermann is an experienced education policy and communications

professional with experience spanning both federal and state government

and policy advocacy organizations. She most recently worked as the Chief

Operating Officer at P2 Public Affairs. Prior to that, she served as an

Assistant Secretary of Education for Governor Glenn Youngkin and worked

as a Special Assistant and Presidential Management Fellow at the Office

of Management and Budget in the first Trump Administration. Madi

received her bachelor’s degree and master of public administration from

the University of Southern California.

Candice Jackson – Deputy General Counsel

Candice

Jackson returns to the U.S. Department of Education to serve as Deputy

General Counsel. Candice served in the first Trump Administration as

Acting Assistant Secretary for Civil Rights, and Deputy General Counsel,

from 2017-2021. For the last few years, Candice has practiced law in

Washington State and California and consulted with groups and

individuals challenging the harmful effects of the concept of "gender

identity" in laws and policies in schools, employment, and public

accommodations. Candice is mom to girl-boy twins Madelyn and Zachary,

age 11.

Joshua Kleinfeld – Deputy General Counsel

Joshua

Kleinfeld is the Allison & Dorothy Rouse Professor of Law and

Director of the Boyden Gray Center for the Study of the Administrative

State at George Mason University’s Scalia School of Law. He writes and

teaches about constitutional law, criminal law, and statutory

interpretation, focusing in all fields on whether democratic ideals are

realized in governmental practice. As a scholar and public intellectual,

he has published work in the Harvard, Stanford, and University of

Chicago Law Reviews, among other venues. As a practicing lawyer, he has

clerked on the D.C. Circuit, Fourth Circuit, and Supreme Court of

Israel, represented major corporations accused of billion-dollar

wrongdoing, and, on a pro bono basis, represented children accused of

homicide. As an academic, he was a tenured full professor at

Northwestern Law School before lateraling to Scalia Law School. He holds

a J.D. in law from Yale Law School, a Ph.D. in philosophy from the

Goethe University of Frankfurt, and a B.A. in philosophy from Yale

College.

Hannah Ruth Earl – Director, Center for Faith-Based and Neighborhood Partnerships

Hannah

Ruth Earl is the former executive director of America’s Future, where

she cultivated communities of freedom-minded young professionals and

local leaders. She previously co-produced award-winning feature films as

director of talent and creative development at the Moving Picture

Institute. A native of Tennessee, she holds a master of arts in religion

from Yale Divinity School.

When

borrowers default on their federal student loans, the U.S. Department

of Education (“Department of Education”) can collect the outstanding

balance through forced collections, including the offset of tax refunds

and Social Security benefits and the garnishment of wages. At the

beginning of the COVID-19 pandemic, the Department of Education paused

collections on defaulted federal student loans.1

This year, collections are set to resume and almost 6 million student

loan borrowers with loans in default will again be subject to the

Department of Education’s forced collection of their tax refunds, wages,

and Social Security benefits.2

Among the borrowers who are likely to experience forced collections are

an estimated 452,000 borrowers ages 62 and older with defaulted loans

who are likely receiving Social Security benefits.3

This

spotlight describes the circumstances and experiences of student loan

borrowers affected by the forced collection of Social Security benefits.4

It also describes how forced collections can push older borrowers into

poverty, undermining the purpose of the Social Security program.5

Key findings

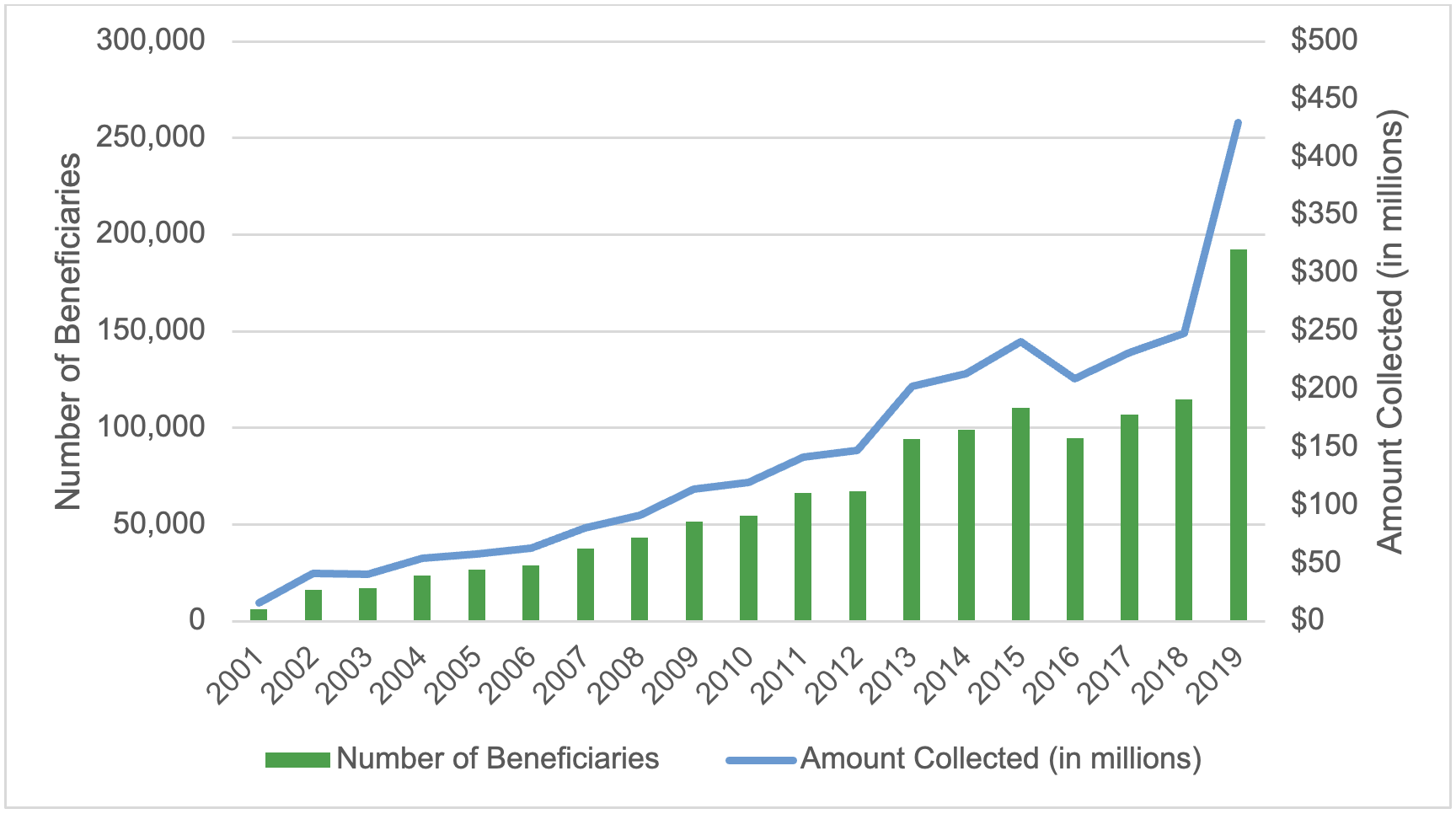

The

number of Social Security beneficiaries experiencing forced collection

grew by more than 3,000 percent in fewer than 20 years; the count is

likely to grow as the age of student loan borrowers trends older.

Between 2001 and 2019, the number of Social Security beneficiaries

experiencing reduced benefits due to forced collection increased from

approximately 6,200 to 192,300. This exponential growth is likely driven

by older borrowers who make up an increasingly large share of the

federal student loan portfolio. The number of student loan borrowers

ages 62 and older increased by 59 percent from 1.7 million in 2017 to

2.7 million in 2023, compared to a 1 percent decline among borrowers

under the age of 62.

The total amount

of Social Security benefits the Department of Education collected

between 2001 and 2019 through the offset program increased from $16.2

million to $429.7 million. Despite the exponential increase in

collections from Social Security, the majority of money the Department

of Education has collected has been applied to interest and fees and has

not affected borrowers’ principal amount owed. Furthermore, between

2016 and 2019, the Department of the Treasury’s fees alone accounted for

nearly 10 percent of the average borrower’s lost Social Security

benefits.

More than one in three

Social Security recipients with student loans are reliant on Social

Security payments, meaning forced collections could significantly

imperil their financial well-being. Approximately 37 percent of the

1.3 million Social Security beneficiaries with student loans rely on

modest payments, an average monthly benefit of $1,523, for 90 percent of

their income. This population is particularly vulnerable to reduction

in their benefits especially if benefits are offset year-round. In 2019,

the average annual amount collected from individual beneficiaries was

$2,232 ($186 per month).

The physical well-being of half of Social Security beneficiaries with student loans in default may be at risk.

Half of Social Security beneficiaries with student loans in default and

collections skipped a doctor’s visit or did not obtain prescription

medication due to cost.

Existing minimum income protections fail to protect student loan borrowers with Social Security against financial hardship.

Currently, only $750 per month of Social Security income—an amount that

is $400 below the monthly poverty threshold for an individual and has

not been adjusted for inflation since 1996—is protected from forced

collections by statute. Even if the minimum protected income was

adjusted for inflation, beneficiaries would likely still experience

hardship, such as food insecurity and problems paying utility bills. A

higher threshold could protect borrowers against hardship more

effectively. The CFPB found that for 87 percent of student loan

borrowers who receive Social Security, their benefit amount is below 225

percent of the federal poverty level (FPL), an income level at which

people are as likely to experience material hardship as those with

incomes below the federal poverty level.

Large

shares of Social Security beneficiaries affected by forced collections

may be eligible for relief or outright loan cancellation, yet they are

unable to access these benefits, possibly due to insufficient

automation or borrowers’ cognitive and physical decline. As many as

eight in ten Social Security beneficiaries with loans in default may be

eligible to suspend or reduce forced collections due to financial

hardship. Moreover, one in five Social Security beneficiaries may be

eligible for discharge of their loans due to a disability. Yet these

individuals are not accessing such relief because the Department of

Education’s data matching process insufficiently identifies those who

may be eligible.

Taken together,

these findings suggest that the Department of Education’s forced

collections of Social Security benefits increasingly interfere with

Social Security’s longstanding purpose of protecting its beneficiaries

from poverty and financial instability.

Introduction

When

borrowers default on their federal student loans, the Department of

Education can collect the outstanding balance through forced

collections, including the offset of tax refunds and Social Security

benefits, and the garnishment of wages. At the beginning of the COVID-19

pandemic, the Department of Education paused collections on defaulted

federal student loans. This year, collections are set to resume and

almost 6 million student loan borrowers with loans in default will again

be subject to the Department of Education’s forced collection of their

tax refunds, wages, and Social Security benefits.6

Among

the borrowers who are likely to experience the Department of

Education’s renewed forced collections are an estimated 452,000

borrowers with defaulted loans who are ages 62 and older and who are

likely receiving Social Security benefits.7

Congress created the Social Security program in 1935 to provide a basic

level of income that protects insured workers and their families from

poverty due to situations including old age, widowhood, or disability.8

The Social Security Administration calls the program “one of the most

successful anti-poverty programs in our nation's history.”9

In 2022, Social Security lifted over 29 million Americans from poverty,

including retirees, disabled adults, and their spouses and dependents.10

Congress has recognized the importance of securing the value of Social

Security benefits and on several occasions has intervened to protect

them.11

This

spotlight describes the circumstances and experiences of student loan

borrowers affected by the forced collection of their Social Security

benefits.12

It also describes how the purpose of Social Security is being

increasingly undermined by the limited and deficient options the

Department of Education has to protect Social Security beneficiaries

from poverty and hardship.

The forced collection of Social Security benefits has increased exponentially.

Federal

student loans enter default after 270 days of missed payments and

transfer to the Department of Education’s default collections program

after 360 days. Borrowers with a loan in default face several

consequences: (1) their credit is negatively affected; (2) they lose

eligibility to receive federal student aid while their loans are in

default; (3) they are unable to change repayment plans and request

deferment and forbearance;13 and (4) they face forced collections of tax refunds, Social Security benefits, and wages among other payments.14

To conduct its forced collections of federal payments like tax refunds

and Social Security benefits, the Department of Education relies on a

collection service run by the U.S. Department of the Treasury called the

Treasury Offset Program.15

Between

2001 and 2019, the number of student loan borrowers facing forced

collection of their Social Security benefits increased from at least

6,200 to 192,300.16

That is a more than 3,000 percent increase in fewer than 20 years. By

comparison, the number of borrowers facing forced collections of their

tax refunds increased by about 90 percent from 1.17 million to 2.22

million during the same period.17

This exponential growth of Social Security offsets between 2001 and 2019 is likely driven by multiple factors including:

Older

borrowers accounted for an increasingly large share of the federal

student loan portfolio due to increasing average age of enrollment and

length of time in repayment. Data from the Department of Education

(which is only available since 2017), show that the number of student

loan borrowers ages 62 and older, increased 24 percent from 1.7 million

in 2017 to 2.1 million in 2019, compared to less than 1 percent among

borrowers under the age of 62.18

A larger number of borrowers, especially older borrowers, had loans in default.

Data from the Department of Education show that the number of student

loan borrowers with a defaulted loan increased by 230 percent from 3.8

million in 2006 to 8.8 million in 2019.19 Compounding these trends is the fact that older borrowers are twice as likely to have a loan in default than younger borrowers.20

Due

to these factors, the total amount of Social Security benefits the

Department of Education collected between 2001 and 2019 through the

offset program increased annually from $16.2 million to $429.7 million

(when adjusted for inflation).21

This increase occurred even though the average monthly amount the

Department of Education collected from individual beneficiaries was the

same for most years, at approximately $180 per month.22

Figure 1: Number of Social Security beneficiaries and total amount collected for student loans (2001-2019)

Source: CFPB analysis of public data from U.S. Treasury’s Fiscal Data portal. Amounts are presented in 2024 dollars.

While the total collected from

Social Security benefits has increased exponentially, the majority of

money the Department of Education collected has not been applied to

borrowers’ principal amount owed. Specifically, nearly three-quarters of

the monies the Department of Education collects through offsets is

applied to interest and fees, and not towards paying down principal

balances.23

Between 2016 and 2019, the U.S. Department of the Treasury charged the

Department of Education between $13.12 and $15.00 per Social Security

offset, or approximately between $157.44 and $180 for 12 months of

Social Security offsets per beneficiary with defaulted federal student

loans.24 As a matter of practice, the Department of Education often passes these fees on directly to borrowers.25

Furthermore, these fees accounted for nearly 10 percent of the average

monthly borrower’s lost Social Security benefits which was $183 during

this time.26

Interest and fees not only reduce beneficiaries’ monthly benefits, but

also prolong the period that beneficiaries are likely subject to forced

collections.

Forced collections are compromising Social Security beneficiaries’ financial well-being.

Forced

collection of Social Security benefits affects the financial well-being

of the most vulnerable borrowers and can exacerbate any financial and

health challenges they may already be experiencing. The CFPB’s analysis

of the Survey of Income and Program Participation (SIPP) pooled data for

2018 to 2021 finds that Social Security beneficiaries with student

loans receive an average monthly benefit of $1,524.27

The analysis also indicates that approximately 480,000 (37 percent) of

the 1.3 million beneficiaries with student loans rely on these modest

payments for 90 percent or more of their income,28

thereby making them particularly vulnerable to reduction in their

benefits especially if benefits are offset year-round. In 2019, the

average annual amount collected from individual beneficiaries was $2,232

($186 per month).29

A

recent survey from The Pew Charitable Trusts found that more than nine

in ten borrowers who reported experiencing wage garnishment or Social

Security payment offsets said that these penalties caused them financial

hardship.30

Consequently, for many, their ability to meet their basic needs,

including access to healthcare, became more difficult. According to our

analysis of the Federal Reserve’s Survey of Household Economic and

Decision-making (SHED), half of Social Security beneficiaries with

defaulted student loans skipped a doctor’s visit and/or did not obtain

prescription medication due to cost.31

Moreover, 36 percent of Social Security beneficiaries with loans in

delinquency or in collections report fair or poor health. Over half of

them have medical debt.32

Figure 2: Selected financial experiences and hardships among subgroups of loan borrowers

Source: CFPB analysis of the Federal Reserve Board Survey of Household Economic and Decision-making (2019-2023).

Social Security recipients

subject to forced collection may not be able to access key public

benefits that could help them mitigate the loss of income. This is

because Social Security beneficiaries must list the unreduced amount of

their benefits prior to collections when applying for other means-tested

benefits programs such as Social Security Insurance (SSI), Supplemental

Nutrition Assistance Program (SNAP), and the Medicare Savings Programs.33

Consequently, beneficiaries subject to forced collections must report

an inflated income relative to what they are actually receiving. As a

result, these beneficiaries may be denied public benefits that provide

food, medical care, prescription drugs, and assistance with paying for

other daily living costs.34

Consumers’

complaints submitted to the CFPB describe the hardship caused by forced

collections on borrowers reliant on Social Security benefits to pay for

essential expenses.35

Consumers often explain their difficulty paying for such expenses as

rent and medical bills. In one complaint, a consumer noted that they

were having difficulty paying their rent since their Social Security

benefit usually went to paying that expense.36

In another complaint, a caregiver described that the money was being

withheld from their mother’s Social Security, which was the only source

of income used to pay for their mother’s care at an assisted living

facility.37

As forced collections threaten the housing security and health of

Social Security beneficiaries, they also create a financial burden on

non-borrowers who help address these hardships, including family members

and caregivers.

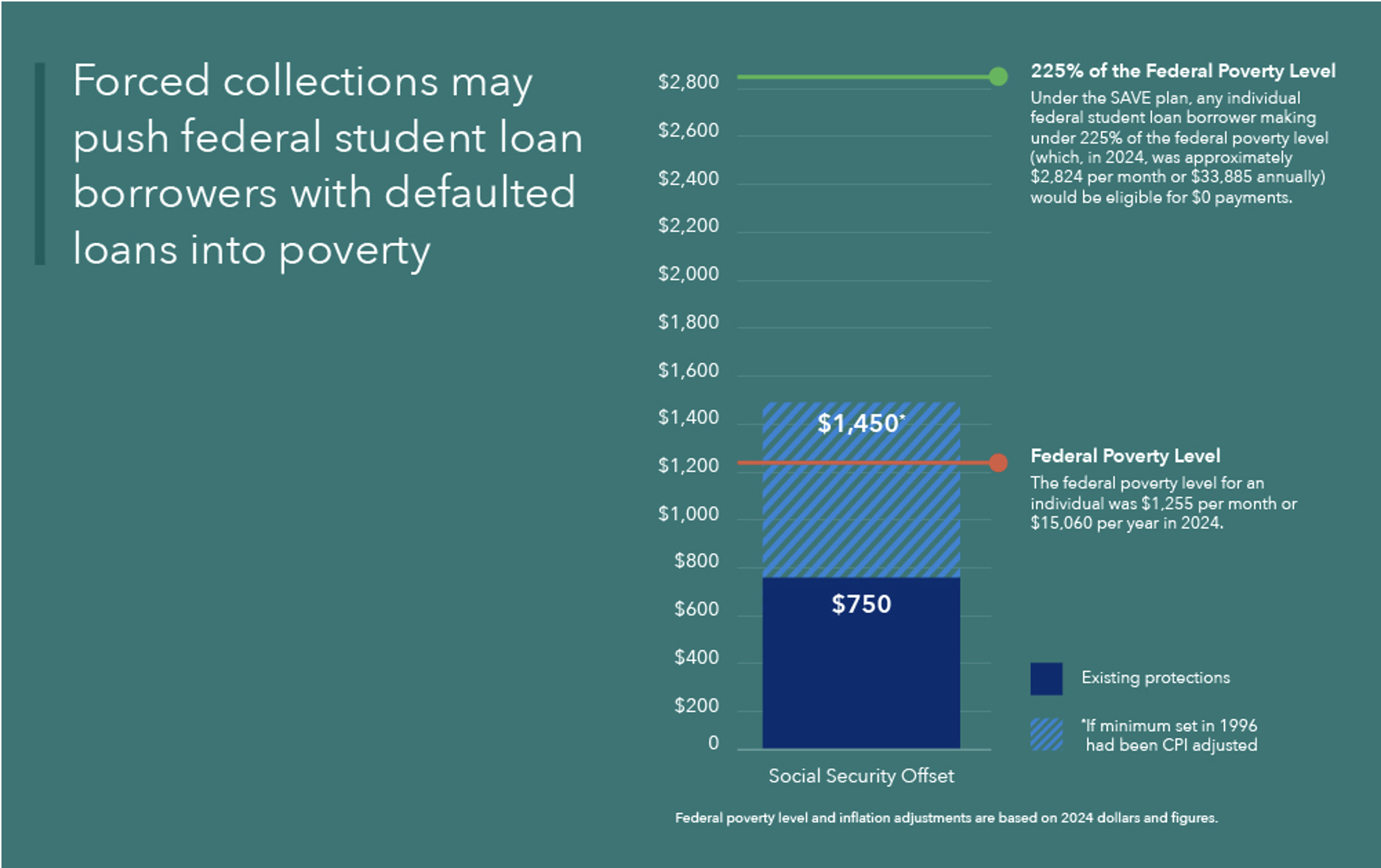

Existing minimum income protections fail to protect student loan borrowers with Social Security against financial hardship.

The

Debt Collection Improvement Act set a minimum floor of income below

which the federal government cannot offset Social Security benefits and

subsequent Treasury regulations established a cap on the percentage of

income above that floor.38

Specifically, these statutory guardrails limit collections to 15

percent of Social Security benefits above $750. The minimum threshold

was established in 1996 and has not been updated since. As a result, the

amount protected by law alone does not adequately protect beneficiaries

from financial hardship and in fact no longer protects them from

falling below the federal poverty level (FPL). In 1996, $750 was nearly

$100 above the monthly poverty threshold for an individual.39

Today that same protection is $400 below the threshold. If the

protected amount of $750 per month ($9,000 per year) set in 1996 was

adjusted for inflation, in 2024 dollars, it would total $1,450 per month

($17,400 per year).40

Figure

3: Comparison of monthly FPL threshold with the current protected

amount established in 1996 and the amount that would be protected with

inflation adjustment

Source: Calculations by the CFPB. Notes: Inflation adjustments based on the consumer price index (CPI).

Even if the minimum protected

income of $750 is adjusted for inflation, beneficiaries will likely

still experience hardship as a result of their reduced benefits.

Consumers with incomes above the poverty line also commonly experience

material hardship.41 This suggests that a threshold that is higher than the poverty level will more effectively protect against hardship.42

Indeed, in determining an income threshold for $0 payments under the

SAVE plan, the Department of Education researchers used material

hardship (defined as being unable to pay utility bills and reporting

food insecurity) as their primary metric, and found similar levels of

material hardship among those with incomes below the poverty line and

those with incomes up to 225 percent of the FPL.43

Similarly, the CFPB’s analysis of a pooled sample of SIPP respondents

finds the same levels of material hardship for Social Security

beneficiaries with student loans with incomes below 100 percent of the

FPL and those with incomes up to 225 percent of the FPL.44

The CFPB found that for 87 percent of student loan borrowers who

receive Social Security, their benefit amount is below 225 percent of

the FPL.45

Accordingly, all of those borrowers would be removed from forced

collections if the Department of Education applied the same income

metrics it established under the SAVE program to an automatic hardship

exemption program.

Existing options for relief from forced collections fail to reach older borrowers.

Borrowers

with loans in default remain eligible for certain types of loan

cancellation and relief from forced collections. However, our analysis

suggests that these programs may not be reaching many eligible

consumers. When borrowers do not benefit from these programs, their

hardship includes, but is not limited to, unnecessary losses to their

Social Security benefits and negative credit reporting.

Borrowers who become disabled after reaching full retirement age may miss out on Total and Permanent Disability

The

Total and Permanent Disability (TPD) discharge program cancels federal

student loans and effectively stops all forced collections for disabled

borrowers who meet certain requirements. After recent revisions to the

program, this form of cancelation has become common for those borrowers

with Social Security who became disabled prior to full retirement age.46 In 2016, a GAO study documented the significant barriers to TPD that Social Security beneficiaries faced.47

To address GAO’s concerns, the Department of Education in 2021 took a

series of mitigating actions, including entering into a data-matching

agreement with the Social Security Administration (SSA) to automate the

TPD eligibility determination and discharge process.48

This process was expanded further with new final rules being

implemented July 1, 2023 that expanded the categories of borrowers

eligible for automatic TPD cancellation.49 In total, these changes successfully resulted in loan cancelations for approximately 570,000 borrowers.50

However,

the automation and other regulatory changes did not significantly

change the application process for consumers who become disabled after

they reach full retirement age or who have already claimed the Social

Security retirement benefits. For these beneficiaries, because they are

already receiving retirement benefits, SSA does not need to determine

disability status. Likewise, SSA does not track disability status for

those individuals who become disabled after they start collecting their

Social Security retirement benefits.51

Consequently,

SSA does not transfer information on disability to the Department of

Education once the beneficiary begins collecting Social Security

retirement.52

These individuals therefore will not automatically get a TPD discharge

of their student loans, and they must be aware and physically and

mentally able to proactively apply for the discharge.53

The

CFPB’s analysis of the Census survey data suggests that the population

that is excluded from the TPD automation process could be substantial.

More than one in five (22 percent) Social Security beneficiaries with

student loans are receiving retirement benefits and report a disability

such as a limitation with vision, hearing, mobility, or cognition.54

People with dementia and other cognitive disabilities are among those

with the greatest risk of being excluded, since they are more likely to

be diagnosed after the age 70, which is the maximum age for claiming

retirement benefits.55

These

limitations may also help explain why older borrowers are less likely

to rehabilitate their defaulted student loans. Specifically, 11 percent

of student loan borrowers ages 50 to 59 facing forced collections

successfully rehabilitated their loans,56 while only five percent of borrowers over the age of 75 do so.57

Figure

4: Number of student loan borrowers ages 50 and older in forced

collection, borrowers who signed a rehabilitation agreement, and

borrowers who successfully rehabilitated a loan by selected age groups

Age Group

Number of Borrowers in Offset

Number of Borrowers Who Signed a Rehabilitation Agreement

Percent of Borrowers Who Signed a Rehabilitation Agreement

Number of Borrowers Successfully Rehabilitated

Percent of Borrowers who Successfully Rehabilitated

50 to 59

265,200

50,800

14%

38,400

11%

60 to 74

184,900

24,100

11%

18,500

8%

75 and older

15,800

1,000

6%

800

5%

Source: CFPB analysis of data provided by the Department of Education.

Shifting demographics of

student loan borrowers suggest that the current automation process may

become less effective to protect Social Security benefits from forced

collections as more and more older adults have student loan debt. The

fastest growing segment of student loan borrowers are adults ages 62 and

older. These individuals are generally eligible for retirement

benefits, not disability benefits, because they cannot receive both

classifications at the same time. Data from the Department of Education

reflect that the number of student loan borrowers ages 62 and older

increased by 59 percent from 1.7 million in 2017 to 2.7 million in 2023.

In comparison, the number of borrowers under the age of 62 remained

unchanged at 43 million in both years.58

Furthermore, additional data provided to the CFPB by the Department of

Education show that nearly 90,000 borrowers ages 81 and older hold an

average amount of $29,000 in federal student loan debt, a substantial

amount despite facing an estimated average life expectancy of less than

nine years.59

Existing exceptions to forced collections fail to protect many Social Security beneficiaries

In

addition to TPD discharge, the Department of Education offers reduction

or suspension of Social Security offset where borrowers demonstrate

financial hardship.60

To show hardship, borrowers must provide documentation of their income

and expenses, which the Department of Education then uses to make its

determination.61

Unlike the Debt Collection Improvement Act’s minimum protections, the

eligibility for hardship is based on a comparison of an individual’s

documented income and qualified expenses. If the borrower has eligible

monthly expenses that exceed or match their income, the Department of

Education then grants a financial hardship exemption.62

The

CFPB’s analysis suggests that the vast majority of Social Security

beneficiaries with student loans would qualify for a hardship

protection. According to CFPB’s analysis of the Federal Reserve Board’s

SHED, eight in ten (82 percent) of Social Security beneficiaries with

student loans in default report that their expenses equal or exceed

their income.63

Accordingly, these individuals would likely qualify for a full

suspension of forced collections. Yet the GAO found that in 2015 (when

the last data was available) less than ten percent of Social Security

beneficiaries with forced collections applied for a hardship exemption

or reduction of their offset.64

A possible reason for the low uptake rate is that many beneficiaries or

their caregivers never learn about the hardship exemption or the

possibility of a reduction in the offset amount.65

For those that do apply, only a fraction get relief. The GAO study

found that at the time of their initial offset, only about 20 percent of

Social Security beneficiaries ages 50 and older with forced collections

were approved for a financial hardship exemption or a reduction of the

offset amount if they applied.66

Conclusion

As

hundreds of thousands of student loan borrowers with loans in default

face the resumption of forced collection of their Social Security

benefits, this spotlight shows that the forced collection of Social

Security benefits causes significant hardship among affected borrowers.

The spotlight also shows that the basic income protections aimed at

preventing poverty and hardship among affected borrowers have become

increasingly ineffective over time. While the Department of Education

has made some improvements to expand access to relief options,

especially for those who initially receive Social Security due to a

disability, these improvements are insufficient to protect older adults

from the forced collection of their Social Security benefits.

Taken

together, these findings suggest that forced collections of Social

Security benefits increasingly interfere with Social Security’s

longstanding purpose of protecting its beneficiaries from poverty and

financial instability. These findings also suggest that alternative

approaches are needed to address the harm that forced collections cause

on beneficiaries and to compensate for the declining effectiveness of

existing remedies. One potential solution may be found in the Debt

Collection Improvement Act, which provides that when forced collections

“interfere substantially with or defeat the purposes of the payment

certifying agency’s program” the head of an agency may request from the

Secretary of the Treasury an exemption from forced collections.67

Given the data findings above, such a request for relief from the

Commissioner of the Social Security Administration on behalf of Social

Security beneficiaries who have defaulted student loans could be